TL;DR:

- Adventure travel insurance uniquely covers high-risk activities typically excluded from standard plans, such as skiing and scuba diving. Choosing the right policy requires verifying detailed activity lists, evacuation limits, and proper procedures during emergencies to ensure claims are approved. Careful policy review and adherence to insurer protocols are essential for reliable coverage on adventure trips.

Adventure travel insurance is a specialized policy that extends standard travel protections to cover high-risk activities typically excluded from conventional plans, including skiing, scuba diving, rock climbing, and skydiving. Where a standard travel policy stops at routine medical emergencies and trip cancellations, adventure coverage explicitly adds protection for injuries and evacuations tied to high-risk activities. Providers like World Nomads, Battleface, and IMG Global each offer policies built around this distinction. If your trip involves anything more physically demanding than a city walking tour, standard coverage almost certainly leaves you exposed.

What is adventure travel insurance and what does it cover?

Adventure travel insurance is defined as a policy that combines the core elements of standard travel insurance with explicit coverage for adventurous and extreme sports activities. Standard policies exclude sports like skydiving, bungee jumping, and white-water rafting, treating them as unacceptable risk. Adventure-specific coverage closes that gap directly.

Core coverage categories

The coverage structure of a typical adventure policy includes:

- Emergency medical treatment: Covers hospital bills, surgery, and physician fees resulting from injuries sustained during a covered activity.

- Emergency evacuation: Pays for helicopter rescues, medical airlifts, and transport to the nearest adequate medical facility.

- Trip cancellation and interruption: Reimburses prepaid, non-refundable costs if you must cancel or cut short your trip due to a covered reason.

- Baggage and equipment: Covers lost, stolen, or damaged gear, including specialized adventure equipment like wetsuits, climbing harnesses, or ski gear.

- Accidental death and dismemberment: Provides a benefit in the most severe outcomes from an activity-related accident.

Emergency medical and evacuation coverage is the most critical distinction. A helicopter evacuation from a remote mountain location can cost $50,000 or more without insurance. That single scenario justifies the entire policy cost.

Standalone policies vs. add-ons

You can purchase adventure coverage as a standalone policy or as a rider added to an existing standard travel plan. Standalone policies from providers like World Nomads tend to offer broader activity lists and higher medical limits. Add-ons are cheaper but often cover a narrower set of activities and lower evacuation limits. If your trip centers on adventure activities rather than occasional excursions, a standalone policy gives you more reliable protection.

Pro Tip: Before purchasing, download the insurer's full activity list and check every planned activity by name. Generic terms like "water sports" or "mountain activities" may not include the specific sport you have in mind.

How insurers define covered activities and what they exclude

Coverage depends heavily on the specific activity list written into your policy and the conditions attached to each activity. Insurers use underwriting categories that map activities to risk tiers, and your eligibility for a claim depends on whether your specific activity falls within a listed and approved category.

How activity tiers work

Insurers like IEC Insurance categorize activities by intensity, geographic constraints, and operational conditions. Recreational scuba diving to 18 meters may be covered, while technical diving beyond 40 meters is excluded. A casual mountain trek at 3,000 meters may be included, while high-altitude mountaineering above 6,000 meters requires a separate endorsement. The mapping between what you plan to do and what the insurer has approved is where most coverage disputes originate.

Common exclusions across policies

| Activity or Condition | Typical Coverage Status |

|---|---|

| Recreational skiing on marked runs | Covered under most adventure policies |

| Freestyle skiing or off-piste skiing | Excluded or requires add-on |

| Scuba diving within recreational depth limits | Covered with certification requirement |

| Technical or solo diving | Excluded by most standard adventure policies |

| Bungee jumping from licensed operators | Covered by select providers |

| Skydiving beyond a set number of jumps | Excluded or limited to tandem jumps |

| Professional or competitive athletics | Excluded across virtually all policies |

| Activities under drug or alcohol influence | Excluded across all policies |

Exclusion lists consistently include professional athletics, injuries sustained while intoxicated, and participation against medical advice. These are non-negotiable across providers. Understanding the difference between a prohibited activity and one that simply requires optional coverage is the key to reading a policy accurately.

Pro Tip: If you plan a less common activity like coasteering, canyoneering, or free solo climbing, call the insurer directly before purchasing. Get written confirmation that your specific activity is covered. A phone call takes five minutes and prevents a denied claim.

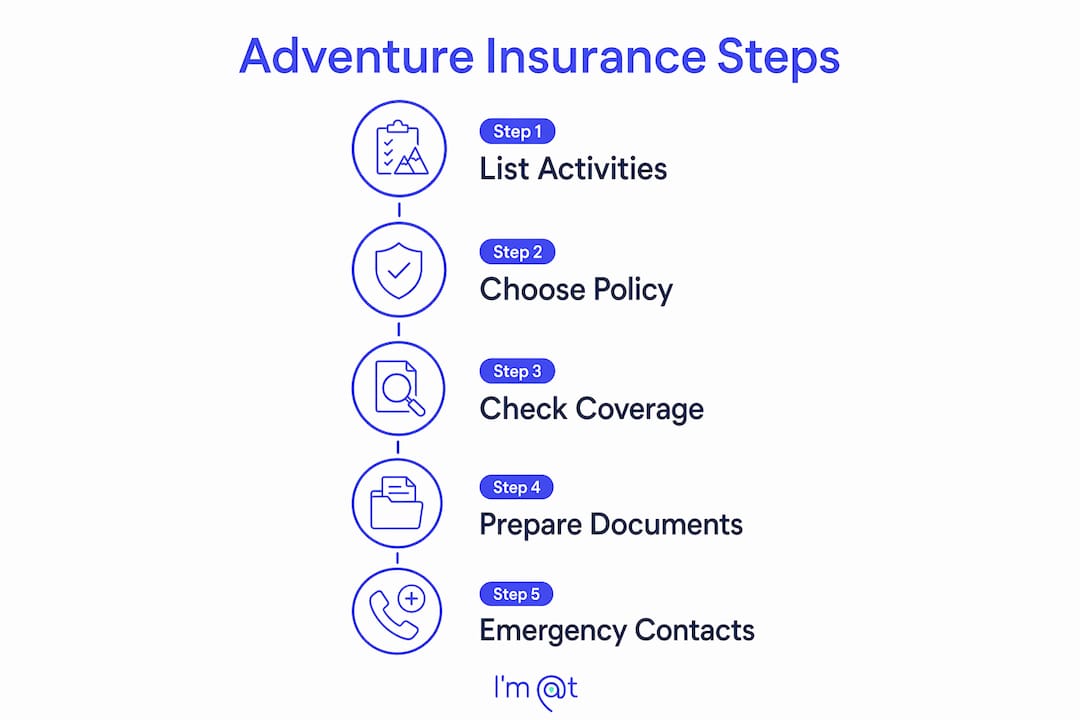

How to choose the right adventure travel insurance policy

Selecting the best adventure insurance for your trip requires matching your specific itinerary to policy terms, not just buying the plan with the most impressive marketing copy. Adventure sports insurance generally costs between $27 and $32 per day for a comprehensive policy, which means a two-week trip runs roughly $380 to $450. That cost is meaningful, so the selection process deserves real attention.

Follow these steps when evaluating policies:

- List every planned activity by its exact name. Include supporting conditions like altitude, depth, and whether you will be guided or independent. Vague descriptions lead to coverage gaps.

- Verify emergency evacuation coverage and limits. Confirm the policy covers evacuation from remote locations and check whether the limit is adequate for your destination. Remote regions in Nepal, Patagonia, or Antarctica carry higher evacuation costs.

- Check medical coverage limits. A minimum of $100,000 in emergency medical coverage is a reasonable baseline for adventure travel. Higher-risk destinations or activities warrant $250,000 or more.

- Compare standalone vs. add-on options. If adventure activities are the core of your trip, a standalone policy from a specialist provider gives you broader protection than a rider on a standard plan.

- Review the assistance services. The best policies include 24/7 emergency assistance lines staffed by medical professionals who coordinate evacuations and hospital admissions in real time.

- Consider Cancel For Any Reason (CFAR) coverage. Standard cancellation covers specific named reasons. CFAR reimburses up to 75% of prepaid costs regardless of reason, which matters when adventure trips involve non-refundable expedition deposits.

- Read the exclusions section in full. This is where the real policy lives. The coverage summary tells you what is included; the exclusions section tells you when that coverage disappears.

When choosing adventure experiences for your trip, build your insurance selection around your confirmed activity list rather than estimating after the fact.

What procedural details determine whether your claim gets paid?

Buying the right policy is only half the equation. How you behave during an emergency determines whether the coverage you paid for actually pays out. Emergency evacuation requires contacting the insurer's assistance service before evacuation expenses are incurred. Failure to do so can void the claim entirely, even when the medical emergency is legitimate and the activity was covered.

Why the approval process matters

Most travelers assume that a covered emergency automatically triggers payment. The reality is that prior approval for evacuations is a contractual requirement, not a formality. If a companion arranges a private helicopter evacuation without contacting the insurer first, the insurer may refuse to reimburse the cost. The policy requires the insurer to coordinate the evacuation, not simply pay for one arranged independently.

Best practices for smooth claims

- Save your insurer's 24/7 emergency assistance number in your phone and write it on a physical card you carry separately.

- Download your policy document offline before departure. Remote locations rarely have reliable internet access during emergencies.

- Photograph all gear and equipment before your trip to support baggage and equipment claims.

- Keep all medical receipts, hospital discharge summaries, and incident reports. Claims without documentation are routinely delayed or denied.

- Notify your insurer of any medical treatment within the timeframe specified in your policy, typically 30 days.

- If you are traveling to a remote location, review the health and safety protocols of your tour operator. Operators with established emergency procedures reduce response time and support insurer coordination.

Effective claims depend on following insurer protocols precisely. The operational bottleneck in adventure travel emergencies is rarely the coverage limit. It is the coordination process between the traveler, the local medical system, and the insurer's assistance team.

Pro Tip: Set your insurer's emergency number as a contact labeled "INSURANCE EMERGENCY" in your phone. In a high-stress situation, you will not remember a number you looked up once six months ago.

Key takeaways

Adventure travel insurance covers what standard policies exclude, and the procedural details of your policy matter as much as the coverage categories themselves.

| Point | Details |

|---|---|

| Specialized coverage is required | Standard travel insurance excludes most adventure sports; a dedicated policy or add-on is necessary. |

| Activity lists define your protection | Coverage is tied to explicitly listed activities; verify every planned sport by name before purchasing. |

| Evacuation approval is mandatory | Contact your insurer's assistance line before evacuation expenses are incurred or risk claim denial. |

| Cost runs $27 to $32 per day | Comprehensive adventure policies are priced higher than standard plans due to elevated risk coverage. |

| CFAR adds meaningful flexibility | Cancel For Any Reason coverage protects non-refundable expedition deposits when standard cancellation terms fall short. |

Why most travelers underestimate what adventure insurance actually demands

I have reviewed dozens of adventure travel insurance policies over the years, and the pattern I see most often is not that travelers skip coverage. It is that they buy a policy, assume they are protected, and never read past the coverage summary page.

The exclusions section is where the real policy lives. I have seen travelers denied claims for skiing off-piste because their policy covered "skiing" without specifying that off-piste required a separate endorsement. I have seen evacuation claims rejected because a well-meaning travel companion arranged a helicopter without calling the insurer first. These are not edge cases. They are predictable outcomes of not reading the document you paid for.

The cost argument also gets misapplied. Travelers sometimes choose the cheapest adventure add-on to save $40 on a $3,000 trip, then discover the evacuation limit is $25,000 when a realistic evacuation from their destination costs $80,000. The adventure tourism risks involved in remote destinations make coverage limits a more important variable than premium price.

My honest advice: treat the policy selection process like you treat gear selection. You would not buy a harness without checking its load rating. Do not buy insurance without checking its evacuation limit, its activity list, and its exclusions. Thirty minutes of reading before your trip is worth more than any coverage summary.

— Mikahil

Find your next adventure and travel protected with Im-at

Im-at connects you with popular adventure activities worldwide, from guided safaris and cultural tours to outdoor expeditions that demand real preparation. Before you book, knowing your coverage is as important as knowing your itinerary. Im-at makes it easy to discover and book experiences across dozens of destinations, so you can plan your trip with confidence. Whether you are heading out on a Cape Town adventure or exploring the Douro Valley, start with the right experience. Explore The Unholy Secrets adventure event and see what Im-at has lined up for travelers who take their trips seriously.

FAQ

What is adventure travel insurance in simple terms?

Adventure travel insurance is a specialized policy that covers medical emergencies, evacuations, and trip cancellations tied to high-risk activities like skiing, scuba diving, and bungee jumping. Standard travel insurance excludes these activities, making a dedicated adventure policy necessary for most active travelers.

Who needs adventure travel insurance?

Any traveler participating in physically demanding or high-risk activities needs adventure travel coverage. This includes skiers, divers, climbers, cyclists, surfers, and anyone booking guided expeditions in remote locations where standard medical infrastructure is limited.

What does adventure insurance typically not cover?

Adventure activity insurance consistently excludes professional or competitive athletics, injuries sustained under the influence of drugs or alcohol, and activities undertaken against medical advice. Many policies also exclude extreme altitude mountaineering and technical diving beyond recreational depth limits unless specifically endorsed.

How much does adventure travel insurance cost?

Comprehensive adventure travel insurance costs approximately $27 to $32 per day depending on the provider and coverage scope. A two-week policy typically runs between $380 and $450, with higher premiums for older travelers or destinations with elevated medical costs.

Can I add adventure coverage to my existing travel insurance?

Many standard travel insurance providers offer adventure sports riders or add-ons that extend coverage to specific high-risk activities. However, standalone policies from specialist providers generally offer broader activity lists and higher evacuation limits, making them the stronger choice for trips centered on adventure activities.